MONTHLY ECONOMIC & INVESTMENT REVIEW:

March 2026 was characterised by a broad-based risk-off environment across global financial markets, driven by a combination of tightening financial conditions, renewed geopolitical uncertainty, and growing concerns around the sustainability of global growth.

Equity markets declined sharply across both developed and emerging markets, with Australian equities underperforming amid global weakness and sensitivity to commodity-linked sectors. Volatility rose materially over the month, reflecting a reassessment of risk premia following a strong start to the year.

Bond markets also weakened modestly, with yields remaining elevated as central banks maintained a cautious stance on policy easing. At the same time, the Australian dollar depreciated meaningfully against the US dollar, reflecting both weaker risk sentiment and a relative shift toward safe-haven currencies.

Overall, March marked a clear shift in market tone — from the constructive and resilient conditions observed earlier in the year to a more fragile environment characterised by heightened volatility, weaker asset prices, and increased macroeconomic uncertainty.

Australian Equities

Australian equities experienced a significant drawdown in March, with the S&P/ASX 200 declining 7.8% on a price return basis and 7.1% on a total return basis. Small capitalisation stocks were particularly weak, with the Small Ordinaries Index falling 11.6%, reflecting their higher sensitivity to growth expectations and risk sentiment.

The decline was broad-based across sectors. Financials came under pressure due to concerns around credit quality and margin compression in a higher-for-longer interest rate environment. At the same time, Materials weakened alongside falling commodity prices and softer demand expectations from China.

The magnitude of the decline highlights the Australian market’s vulnerability to global macro conditions, particularly given its cyclical sector composition and exposure to external demand.

Global Developed Equities

Global developed equity markets also declined during March. The S&P 500 fell 5.1%, while developed market equities (as proxied by IWLD) declined 5.5%.

Market weakness was driven by several key factors. First, expectations for near-term monetary policy easing were pushed back, as inflation — particularly in services — remained more persistent than anticipated. Second, concerns emerged around the sustainability of earnings growth following a strong reporting period, particularly in sectors exposed to artificial intelligence-related capital expenditure.

While market leadership had broadened in previous months, March saw a more indiscriminate sell-off across both growth and value sectors, indicating a broader de-risking by investors.

Emerging Markets

Emerging market equities underperformed developed markets, with returns of -6.6% for the month.

China remained a key driver of weakness, with ongoing structural challenges in the property sector and subdued consumer demand weighing on investor sentiment. Despite continued policy support, including infrastructure spending and targeted stimulus measures, confidence in the sustainability of China’s recovery remained fragile.

Capital flows into emerging markets also weakened as global investors reduced risk exposure and rotated toward developed market safe-haven assets.

Real Assets – Property & Infrastructure

Real assets continue to play an important role in portfolio construction, providing income generation, diversification benefits and, in certain cases, inflation-linked cash flows. However, performance across the sector has become increasingly bifurcated, particularly between listed and unlisted exposures, as well as across subsectors within property and infrastructure.

Listed real estate, particularly in Australia, experienced significant weakness during March, reflecting its sensitivity to elevated bond yields and tightening financial conditions. Higher discount rates continue to weigh on valuations, while refinancing risks and pressure on asset values remain key concerns. Global listed REITs have demonstrated relatively better resilience, supported by sector diversification and exposure to structurally supported segments such as logistics and data centres, although they remain vulnerable to further interest rate volatility.

In contrast, unlisted real estate continues to exhibit more stable performance, underpinned by appraisal-based valuations and longer lease structures. However, this stability should be viewed with caution, as valuation adjustments tend to lag listed markets. As such, there remains a risk of downward revaluations in certain segments, particularly in office and retail, where structural and cyclical pressures persist.

Infrastructure remains the highest conviction allocation within real assets. Both listed and unlisted infrastructure assets benefit from relatively stable and predictable cash flows, often supported by regulated or contracted revenue streams. In the current environment, infrastructure’s pricing power and partial inflation linkage provide a degree of protection against macroeconomic uncertainty. Listed infrastructure has demonstrated relative resilience during recent market volatility, while unlisted infrastructure continues to deliver consistent income and low volatility characteristics.

Fixed Income & Interest Rates

Fixed income markets experienced modest declines during March, with Australian government bonds returning –1.7% and global bonds (hedged) returning –2.3%.

Bond yields remained elevated as central banks continued to signal a cautious approach to policy easing. While inflation has moderated from peak levels, progress has been uneven, particularly in services and wage-driven components.

The repricing of interest rate expectations — particularly the delay in anticipated rate cuts — contributed to negative bond returns during the month. Additionally, concerns around fiscal deficits and increased sovereign issuance in major economies also placed upward pressure on yields.

Credit markets remained relatively resilient, although spreads widened modestly as risk sentiment deteriorated.

Commodities & Currencies

Commodity markets were mixed during March, with gold declining 9.0% and broader industrial commodity prices also under pressure.

The decline in gold reflects a combination of factors, including a stabilisation in real yields and a moderation in safe-haven demand following earlier geopolitical-driven gains. Industrial commodities weakened in response to softer global growth expectations and continued uncertainty around Chinese demand.

The Australian dollar depreciated significantly over the month, falling 3.6% against the US dollar. This reflects both a deterioration in global risk sentiment and a relative shift toward the US dollar as a safe-haven currency.

Currency movements were also influenced by diverging monetary policy expectations, with the Federal Reserve maintaining a more hawkish stance relative to other central banks.

Volatility & Market Sentiment

Market volatility increased sharply during March, with the VIX rising 27.1% over the month.

The rise in volatility reflects a shift in investor sentiment from complacency toward heightened caution. Following a period of strong performance and relatively low volatility, markets became more sensitive to downside risks, including macroeconomic uncertainty, policy risks and geopolitical developments.

Elevated volatility is consistent with a transition phase in markets, where investors reassess both growth expectations and valuation levels.

Global Macroeconomic Overview

The global macroeconomic backdrop remains mixed. While economic growth has remained relatively resilient, particularly in the United States, there are increasing signs of moderation.

Labour markets remain tight, supporting consumption, but forward-looking indicators such as manufacturing activity and business confidence suggest a gradual slowdown in economic momentum.

Inflation continues to decline, but at a slower pace than expected. Services inflation remains sticky, reinforcing central banks’ cautious stance on policy easing. The Blockade of the Straits of Hormuz will only add to inflationary concerns as oil supply chains are impeded and prices remain elevated for longer.

Corporate earnings have remained broadly robust; however, there is increasing dispersion across sectors. Companies exposed to cyclical demand and global trade are experiencing pressure, while more defensive sectors are demonstrating greater resilience.

Central Bank Policy

Monetary policy developments remained a key driver of market performance in March, with several central banks either implementing further policy tightening or reinforcing a clear tightening bias, contributing to a reassessment of the global interest rate outlook.

In Australia, the Reserve Bank of Australia increased the official cash rate by 25 basis points to 4.10% during March, extending its tightening cycle following persistent inflationary pressures. The decision reflected ongoing strength in the labour market and continued stickiness in services inflation, with the Bank emphasising that further tightening may be required to ensure inflation returns to target. This contributed to renewed pressure on domestic interest rate-sensitive sectors, including property and small-cap equities.

In the United States, the Federal Reserve held its federal funds rate steady at 3.50%–3.75% during the month. However, the tone of communication remained cautious, with policymakers highlighting persistent services inflation and ongoing labour market strength. As a result, market expectations for the timing and magnitude of rate cuts were pushed further out, with investors increasingly pricing a delayed and gradual easing cycle.

Similarly, the European Central Bank and the Bank of England both kept policy rates unchanged during March, reflecting a shared concern that inflation, while moderating, remains above target levels across developed economies.

The key development for markets was therefore not a shift in policy rates themselves, but a repricing of the expected path of future policy. The persistence of inflation — particularly in services — has led central banks to adopt a more cautious stance, reinforcing the “higher-for-longer” narrative.

This shift in expectations was a major contributor to market performance during the month. Equity valuations came under pressure as discount rates remained elevated, while bond markets struggled to rally meaningfully given the reduced likelihood of near-term rate cuts. Overall, the policy backdrop continues to act as a constraint on risk asset performance, with markets increasingly sensitive to any deviation in inflation or growth data that may alter the trajectory of monetary policy.

OUTLOOK

The investment outlook has become more cautious following the sharp market correction in March, which underscored the increasing sensitivity of asset prices to macroeconomic and policy developments. While the global economy continues to demonstrate underlying resilience, the combination of elevated interest rates, moderating growth and heightened geopolitical risks suggests that volatility is likely to remain a defining feature of markets in the near term.

The recent repricing across equity markets reflects a clear shift in investor sentiment, as participants reassess both the sustainability of earnings growth and appropriate valuation levels within a higher discount rate environment. Although corporate fundamentals remain broadly intact, the margin for error has narrowed materially, particularly in sectors exposed to cyclical demand and global trade dynamics. At the same time, the delayed and uncertain timing of monetary policy easing reinforces the view that financial conditions will remain restrictive, limiting the potential for a sustained recovery in risk assets in the near term.

In this environment, portfolio construction requires a disciplined and risk-aware approach. Diversification across asset classes remains critical, particularly given the reduced effectiveness of traditional defensive assets observed during the month. There is an increased emphasis on quality across both equities and fixed income, favouring businesses and issuers with strong balance sheets, resilient cash flows and the ability to withstand a more challenging macroeconomic backdrop. Real assets, particularly infrastructure, continue to offer attractive diversification benefits, supported by stable income streams and partial insulation from short-term market volatility.

The correction in March may present selective opportunities as valuations adjust and dislocations emerge across markets; however, a cautious stance remains warranted until there is greater clarity on the trajectory of inflation, central bank policy and global growth. Maintaining elevated liquidity and preserving portfolio flexibility will be essential in allowing investors to respond effectively to evolving conditions. Overall, while the medium-term outlook remains constructive, the near-term environment calls for a measured and adaptive approach to asset allocation.

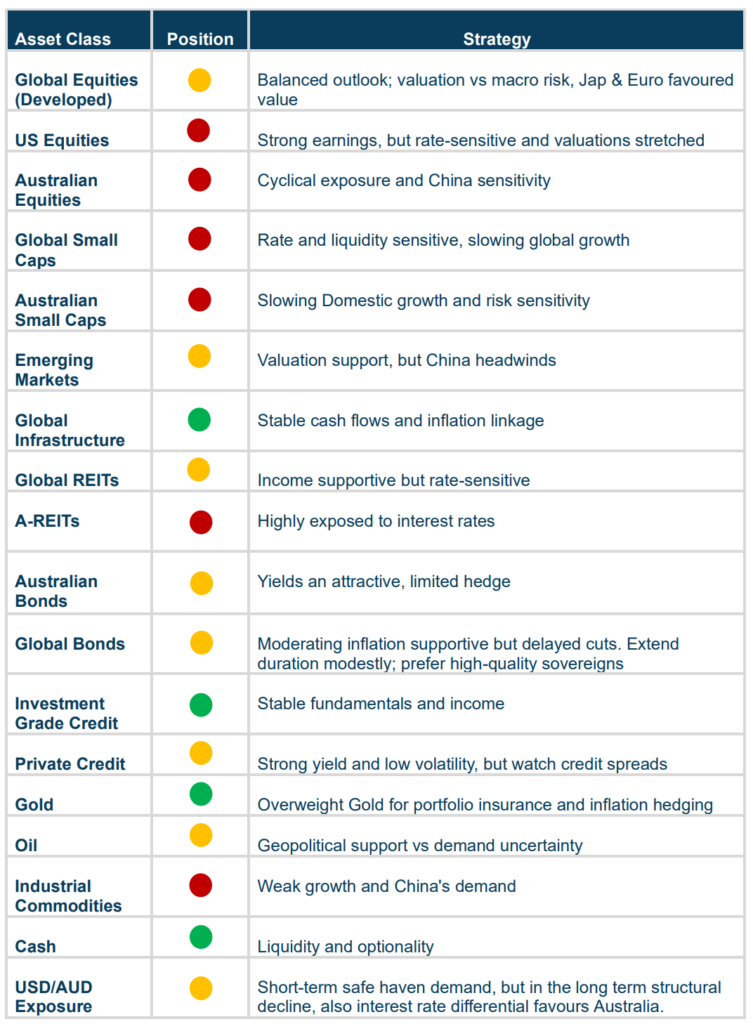

PORTFOLIO STRATEGY & ASSET ALLOCATION