MONTHLY ECONOMIC & INVESTMENT REVIEW:

May 2026 was characterised by a broad improvement in global risk sentiment, with equity markets continuing to recover from the volatility experienced through March and early April. The recovery was led by global developed equities and emerging markets, supported by resilient earnings, improving confidence in the global growth outlook and renewed enthusiasm for artificial intelligence-related investment themes.

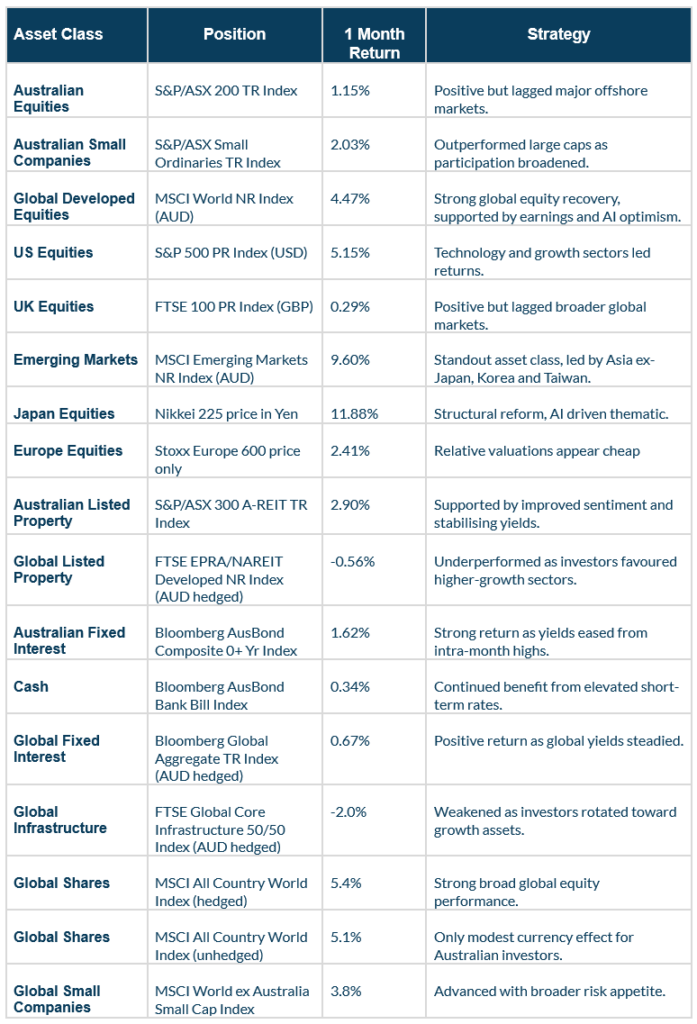

The S&P 500 rose 5.15% in May, underwritten by renewed strength in technology and growth sectors. On a broader basis, the MSCI World Index returned 4.47% in AUD terms, while the MSCI All Country World Index rose 5.4% on a hedged basis and 5.1% unhedged — reflecting only modest currency effects for Australian investors this month. Japanese equities were among the strongest-performing developed markets during May, rising 11.8% as investors responded positively to ongoing corporate governance reforms, robust earnings growth and Japan’s growing importance within global semiconductor and artificial intelligence supply chains, reinforcing our decision to favour Japan as an overweight position. Emerging markets were also a standout performer, with the MSCI Emerging Markets Index rising 9.6%. This was primarily driven by Korea and Taiwan — where semiconductor and AI supply-chain exposure remained the dominant theme. China, by contrast, declined over the month, underscoring the uneven nature of the broader EM rally and reinforcing our decision to remain negative on China with an underweight allocation.

Australian equities also delivered positive returns, although the domestic market lagged major offshore markets. The S&P/ASX 200 Total Return Index rose 1.15%, while Australian small companies outperformed large caps with the S&P/ASX Small Ordinaries Total Return Index gaining 2.03%. Sector performance was uneven, with materials benefiting from stronger copper and electrification-linked demand themes, while healthcare and energy were weaker over the month.

Real assets presented a more mixed picture than in recent months. Global listed property (FTSE EPRA/NAREIT Developed, hedged) declined modestly by 0.56% after April’s gains, while global listed infrastructure (FTSE Global Core Infrastructure 50/50, hedged) fell 2.0% as investors rotated toward higher-growth sectors and reduced exposure to more defensive assets following the strong recovery of recent months. Domestically, however, Australian A-REITs were the standout real asset performer, with the S&P/ASX 300 A-REIT Index rising 2.9% as softer inflation and labour market data led investors to materially scale back expectations for further RBA rate increases.

Fixed income markets also produced positive returns as bond yields eased from intra-month highs. Australian bonds were particularly strong, with the Bloomberg AusBond Composite Index rising 1.62%, while global bonds hedged into Australian dollars returned 0.67%. Overall, May represented a more constructive month for diversified portfolios, although the performance mix favoured growth-oriented assets over traditional defensives such as infrastructure and global listed property.

Australian Equities

Australian equities delivered a positive but comparatively modest return during May, with the S&P/ASX 200 Total Return Index gaining 1.15%. This was a constructive outcome following the volatility experienced earlier in the year, although the local market lagged global developed and emerging market equities. Performance was supported by improving risk appetite, better sentiment toward cyclical sectors and a stronger contribution from materials stocks.

Materials were a key source of strength as copper prices and broader industrial commodity sentiment improved. Investor interest in electrification, data centres and AI-related infrastructure spending continued to support the longer-term demand outlook for selected resources exposures. Consumer discretionary and real estate also benefited from the improvement in risk sentiment, helped by expectations that the domestic economy may slow without entering a more severe downturn.

Healthcare and energy were among the weaker sectors. Healthcare was pressured by company-specific earnings concerns, while energy gave back some of its earlier strength as oil prices eased from geopolitical risk-driven highs. Australian small companies outperformed large caps, rising 2.03%, reflecting broader participation across the market and some recovery in more domestically sensitive names. Despite this improvement, small caps remain more exposed to refinancing costs, domestic demand and earnings downgrades than larger companies.

Our view on Australian equities is upgraded from underweight to neutral. Valuations are more reasonable than in the United States and the market offers attractive income characteristics. However, the domestic market remains exposed to China, commodity prices, household spending pressure and the lagged impact of higher interest rates.

Global Developed Equities

Global developed equities delivered strong returns during May, with the MSCI World Index rising 4.47% in Australian dollar terms. The United States again led the recovery, with the S&P 500 rising 5.15% in US dollar terms. Performance was supported by resilient corporate earnings, stronger risk appetite and renewed enthusiasm for technology and artificial intelligence-related capital expenditure.

The key feature of the month was the continued preference for quality growth companies with strong balance sheets, earnings visibility and exposure to structural investment themes. Technology and communication services remained the major beneficiaries, as investors continued to price in strong demand for semiconductors, cloud computing, data centres and AI infrastructure. This reinforces the view that AI-related investment is not merely a short-term market narrative, but an increasingly important driver of corporate earnings and capital spending.

European and Japanese markets also delivered positive returns, with investors continuing to show interest in non-US developed markets. Europe remains supported by attractive relative valuations, although underlying economic momentum is still subdued. Japan continues to benefit from corporate governance reform, improving capital discipline and a more shareholder-friendly corporate environment.

We upgrade global developed equities to a modest overweight. The strength of earnings momentum and the durability of AI-related investment justify a more constructive stance. However, the upgrade is selective rather than broad-based. Valuation discipline remains important, particularly within US mega-cap technology where market leadership remains concentrated and expectations are elevated.

Emerging Markets

Emerging markets were the standout asset class during May, with the MSCI Emerging Markets Index rising 9.60% in Australian dollar terms. This strong result reflected improving global risk appetite and significant strength across Asia ex-Japan, particularly Korea and Taiwan, where semiconductor and AI supply-chain exposure remained highly supportive.

The rally in emerging markets was not uniform. China declined during the month, highlighting the uneven nature of the asset class and the continuing challenge of weaker consumer confidence, property sector stress and a still-fragile domestic growth outlook. The divergence between China and other Asian markets remains an important feature of the current environment.

Outside China, the outlook for selected emerging markets has improved. Economies linked to semiconductor production, manufacturing relocation and domestic consumption recovery continue to offer attractive medium-term opportunities. Valuations also remain compelling relative to developed markets, particularly where earnings revisions are stabilising.

We maintain a neutral position in emerging markets but recommend a more selective approach within the allocation. Exposure should favour Asia ex-China, quality companies, semiconductor supply-chain beneficiaries and countries with improving domestic fundamentals. China remains a key risk and should not be treated as a broad cyclical recovery trade until evidence of a more durable improvement emerges.

Real Assets – Property & Infrastructure

Real assets produced mixed outcomes during May and did not participate as strongly in the broader risk rally. Australian listed property was positive, with the S&P/ASX 300 A-REIT Total Return Index rising 2.90%. The sector benefited from improving sentiment toward income-oriented assets and signs that domestic bond yields were stabilising. However, refinancing costs and weaker commercial property fundamentals remain important headwinds.

Global listed property was weaker, with the FTSE EPRA/NAREIT Developed Index hedged into Australian dollars declining 0.56%. This was a notable change from April, when listed property had recovered strongly from earlier weakness. The May result reflects the market’s preference for higher-growth sectors and reduced demand for more defensive, income-oriented exposures during a risk-on month.

Infrastructure also weakened, with the FTSE Global Core Infrastructure 50/50 Index hedged declining approximately 2.0%. This underperformance does not change the medium-term investment case for infrastructure, but it does highlight the asset class’s tendency to lag during periods when investors aggressively rotate toward growth equities. Infrastructure remains supported by contracted cash flows, inflation linkage and long-term structural demand from electrification, energy security and digital infrastructure.

Our view on infrastructure remains positive despite the monthly decline. However, we reduce the near-term tactical conviction slightly to reflect the market’s current preference for growth assets. Listed real estate remains neutral overall, while Australian REITs remain vulnerable to refinancing costs and valuation risk in office-related exposures.

Fixed Income & Interest Rates

Fixed income markets delivered positive returns in May as bond yields eased from their intra-month highs. Australian fixed interest performed particularly well, with the Bloomberg AusBond Composite 0+ Year Index rising 1.62%. Global bonds also advanced, with the Bloomberg Global Aggregate Bond Index hedged into Australian dollars returning 0.67%.

The improvement in bond markets was supported by softer inflation data and weaker labour market conditions, which led investors to scale back expectations for additional interest rate increases. This marked an important shift from earlier in the year, when inflation concerns and renewed central bank tightening had weighed on duration-sensitive assets.

Credit markets also edged higher, supported by tighter global credit spreads and broadly stable corporate fundamentals. Investment grade credit remains attractive on a risk-adjusted basis, offering meaningful income without requiring excessive exposure to lower-quality issuers. High yield performed positively, but spreads remain relatively tight, reducing the margin of safety if growth weakens.

We maintain a neutral to modestly positive view on high-quality fixed income. Starting yields remain attractive and bonds have regained some of their defensive characteristics. However, duration exposure should remain measured until there is greater confidence that inflation is sustainably returning to target.

Commodities & Currencies

Commodity markets were mixed during May. Industrial commodities, particularly copper, remained supported by expectations of stronger demand from electrification, grid investment, data centres and artificial intelligence infrastructure. These structural themes continue to provide medium-term support for selected metals despite ongoing uncertainty around Chinese construction demand.

Oil prices eased from earlier strength as immediate fears of supply disruption moderated. This helped improve broader risk sentiment and reduced some of the inflation pressure that had emerged during periods of heightened geopolitical tension. Nevertheless, energy markets remain highly sensitive to developments in the Middle East and any renewed disruption to major shipping routes or supply channels could quickly reintroduce inflationary pressure.

Gold consolidated during the month as safe-haven demand moderated and investors rotated toward risk assets. The short-term decline does not alter the strategic case for gold. Elevated geopolitical uncertainty, central bank buying, fiscal sustainability concerns and the risk of renewed inflation shocks continue to justify a positive medium-term allocation.

The Australian dollar experienced only modest currency effects for global equity investors over the month. Currency exposure remains a balancing tool within portfolios, with the AUD sensitive to global risk appetite, commodity prices and interest rate differentials.

Volatility & Market Sentiment

Market volatility declined during May as investors became more comfortable with the global growth outlook and geopolitical risks eased relative to earlier in the year. Risk appetite improved materially, with investors favouring equities, technology, emerging markets and other growth-sensitive assets.

The recovery was supported by resilient earnings and a perception that the global economy remains capable of achieving a soft landing. The strongest capital flows were directed toward sectors with clear structural growth drivers, especially AI-linked technology and semiconductor supply chains.

Despite the improvement in sentiment, the market backdrop remains fragile. Valuations in parts of the US equity market now embed optimistic earnings assumptions, while geopolitical risks and inflation uncertainty have not disappeared. The decline in volatility should therefore be interpreted as an improvement in conditions rather than a return to a low-risk environment.

Global Macroeconomic Overview

The global economic backdrop in May remained characterised by slowing but positive growth, moderating inflation and restrictive monetary policy settings. The United States continued to demonstrate resilience, supported by earnings strength, household spending and business investment linked to technology infrastructure. However, forward-looking indicators still point to a gradual loss of momentum.

Europe remains more fragile, with subdued manufacturing activity and uneven consumer demand. However, attractive valuations and lower energy pressure have supported financial market performance. Japan continues to benefit from domestic reform momentum and improving corporate behaviour, even as currency and inflation dynamics remain important considerations.

China remains the main source of macroeconomic uncertainty. Policy support has helped stabilise parts of the economy, but the property sector, weak consumer confidence and subdued private investment continue to weigh on the outlook. The fact that China declined while broader emerging markets rallied highlights the importance of separating China-specific risks from opportunities elsewhere in emerging markets.

The inflation outlook improved modestly during May as energy prices eased and bond yields stabilised. However, central banks remain cautious because services inflation and wages remain sticky in several economies. The key macro conclusion is that the global economy remains resilient enough to support earnings, but not strong enough to remove the risk of policy error or renewed volatility.

Central Bank Policy

Monetary policy remained a central driver of market behaviour during May. In Australia, the Reserve Bank’s recent tightening cycle continued to influence household cash flows and market expectations. However, softer inflation data and weaker labour market conditions during the month led investors to reduce expectations for further near-term interest rate increases.

This represents an important shift in the domestic policy backdrop. While policy remains restrictive and the RBA is unlikely to declare victory on inflation, markets are increasingly questioning whether additional tightening will be required. This helped support Australian bonds and contributed to improved sentiment toward interest-rate-sensitive assets such as listed property.

Globally, major central banks maintained a cautious and data-dependent stance. The US Federal Reserve continued to emphasise the need for sustained progress on inflation before easing policy, while the European Central Bank and Bank of England remained similarly cautious. Markets increasingly expect policy rates to be close to cyclical peaks, but the timing of future cuts remains uncertain.

Overall, the policy backdrop is becoming less hostile for diversified portfolios, but not yet clearly supportive. Investors should therefore avoid assuming an aggressive easing cycle and instead position for a prolonged period of restrictive but more stable policy settings.

OUTLOOK

The investment outlook has improved following the strong recovery in global equities and the stabilisation in bond markets during May. The combination of resilient earnings, moderating inflation and easing bond yields provides a more constructive foundation for diversified portfolios than was evident during the March correction.

However, the improvement in markets also requires discipline. Equity valuations have recovered quickly, particularly in the United States, and market leadership remains concentrated in companies benefiting from AI-related investment themes. While these themes are powerful and increasingly supported by earnings, the concentration of returns increases vulnerability to disappointment.

Portfolio construction should therefore remain balanced. We favour a modest overweight to global developed equities, with a preference for quality companies, AI infrastructure beneficiaries and selective exposure to Japan and Europe. Emerging markets should remain neutral but more selective, with a preference for Asia ex-China and semiconductor supply-chain exposure. Australian equities were upgraded to neutral as valuations remain relatively attractive compared to global peers and the May rally became increasingly broad-based, with performance extending beyond the major banks and miners into small companies, consumer discretionary stocks and real estate. This suggests improving investor confidence in both corporate earnings and the domestic economic outlook, but the outlook remains constrained by household pressure and China sensitivity.

Fixed income is now more attractive as a source of income and diversification. We favour high-quality sovereign bonds and investment grade credit, while avoiding excessive exposure to lower-quality credit where spreads appear tight. Infrastructure remains a high-conviction medium-term allocation, although the short-term environment may favour growth equities. Gold remains a strategic hedge against geopolitical risk and renewed inflation volatility. Cash continues to provide liquidity and optionality in an environment where market conditions can change quickly.

Overall, May reinforced that the market recovery is real but selective. The medium-term outlook is constructive, but the appropriate response is not to abandon risk management. A diversified portfolio with exposure to quality growth, defensive income, real assets and liquidity remains the most appropriate strategy for the current environment.

CURRENT PORTFOLIO STRATEGY & ASSET ALLOCATION

The following tactical positioning reflects the improvement in market sentiment during May, the stronger performance of global equities and emerging markets, the positive contribution from fixed income, and the relative underperformance of infrastructure and global listed property during the month. The asset class performance data supporting these conclusions is set out in Appendix A.

APPENDIX A – ASSET CLASS PERFORMANCE SUMMARY

(MAY 2026)