Executive Summary

February was characterised by strong performance in Australian equities, rising geopolitical tensions and growing debate around the structural implications of artificial intelligence for global markets. Australian equities materially outperformed global peers, supported by strong earnings from banks and resource companies and continued resilience in the domestic labour market.

The Reserve Bank of Australia (RBA) increased the official cash rate by 25 basis points to 3.85%, reflecting persistent inflation pressures and a labour market that remains tighter than expected. Headline CPI remains above the RBA’s 2–3% target range, reinforcing the central bank’s concern that inflation expectations could become entrenched.

Globally, equity markets were mixed. Developed market equities declined modestly in AUD terms, while emerging markets delivered strong returns. Market leadership continued to broaden away from US mega-cap technology companies as investors reassessed valuation levels and the implications of AI-driven disruption.

Bond markets rallied over the month as government bond yields declined across most developed economies. The US 10‑year Treasury yield fell below 4%, reflecting moderating inflation data and a more cautious outlook for global growth.

Geopolitical developments also emerged as an important market driver. Military strikes by the United States and Israel on Iran raised concerns about potential disruptions to global energy supply and shipping through the Strait of Hormuz.

Despite these uncertainties, the global economy continues to demonstrate resilience. Corporate earnings remain robust and financial conditions remain broadly supportive of risk assets.

Australian Equities

Australian equities delivered strong returns in February, with the S&P/ASX 200 Accumulation Index rising approximately 4% for the month, significantly outperforming most global equity markets.

Performance was driven primarily by the Financials and Materials sectors. Bank earnings proved stronger than expected, supported by resilient credit growth, stable margins and relatively low bad debt levels. Mining companies also benefited from rising commodity prices, particularly gold and base metals.

By contrast, the Health Care and Information Technology sectors were the largest detractors as investors rotated away from long‑duration growth companies toward cyclicals and value stocks. Concerns around the potential impact of artificial intelligence on software business models also contributed to the technology sector’s underperformance.

Small capitalisation companies lagged large caps during the month, reversing some of their recent period of outperformance. Australia’s reporting season was broadly constructive overall, although result‑day volatility remained elevated.

Global Developed Equities

Global developed equity markets delivered mixed returns during February. The MSCI World Index declined modestly in AUD terms (-1.0%), while the S&P 500 fell slightly during the month (-0.9%).

Corporate earnings remained broadly supportive. Approximately three‑quarters of S&P 500 companies reported results ahead of analyst expectations, with aggregate earnings growth for 2025 tracking well above earlier forecasts.

However, leadership within equity markets continued to rotate. Value and cyclical sectors outperformed growth companies, reflecting elevated valuations within technology stocks and uncertainty surrounding the long‑term implications of AI‑driven productivity gains.

Outside the United States, several developed markets performed strongly, particularly the UK and Japan, supported by fiscal stimulus expectations and improving corporate governance reforms.

Emerging Markets

Emerging market equities were among the strongest performing asset classes in February (+3.7%). Attractive valuations, supportive monetary conditions and stabilising commodity prices helped drive the sector’s outperformance relative to developed markets.

China’s economic data remained mixed. Manufacturing activity contracted modestly during the month, reflecting seasonal weakness around the Lunar New Year and continued challenges within the property sector.

While infrastructure investment has provided some support to economic activity, consumer demand remains subdued and deflationary pressures persist. Despite these challenges, emerging markets continue to benefit from improving relative growth prospects and supportive policy settings.

Listed Real Assets

Real assets delivered divergent returns during February. Australian listed property declined (-3.3%) as higher domestic interest rates continued to pressure long‑duration assets.

In contrast, international listed property and global infrastructure delivered strong gains (7.1%) as global bond yields declined. Infrastructure assets in particular benefited from attractive earnings yields, stable cash flow characteristics and continued investor demand for defensive income‑generating exposures.

Fixed Income

Bond markets delivered positive returns during February as government bond yields declined across most major economies.

The US 10‑year Treasury yield fell significantly as inflation data moderated and geopolitical risks increased. Australian government bond yields also declined during the month despite the RBA’s decision to increase the cash rate.

Credit markets remained stable overall. Spreads widened modestly but corporate balance sheets remain strong and default risks remain relatively contained.

Commodities & Currencies

Commodity markets generally strengthened during February. Gold prices rose strongly in February, gaining approximately 7.9% over the month, supported by falling real bond yields, heightened geopolitical tensions and continued central bank buying, reinforcing gold’s role as a strategic portfolio diversifier and hedge against macroeconomic uncertainty.

Oil prices also increased as tensions in the Middle East raised concerns about potential supply disruptions. Industrial metals delivered moderate gains, while iron ore softened slightly following seasonal demand weakness in China.

The Australian dollar strengthened modestly during the month, supported by higher domestic interest rates and stronger commodity prices.

Global Macroeconomic Overview

The global economy continues to demonstrate resilience despite tightening financial conditions and geopolitical uncertainty.

In the United States, labour market conditions remain strong with payroll growth exceeding expectations and unemployment remaining relatively low. Inflation has continued to moderate gradually, although services inflation remains persistent.

Corporate earnings globally remain robust, though there is increasing divergence between industries benefiting from artificial intelligence investment and those potentially threatened by automation.

In Australia, economic conditions remain broadly stable. Employment growth continues and unemployment remains low, reinforcing the RBA’s view that inflation risks remain skewed to the upside.

Central Bank Policy

Monetary policy developments were a key focus for investors during February. The Reserve Bank of Australia increased the cash rate to 3.85%, marking its first-rate hike since 2023. The central bank emphasised that inflation remains above target and that further tightening may be required should inflation prove persistent.

Globally, other major central banks maintained relatively stable policy settings. The US Federal Reserve held rates steady while the European Central Bank and Bank of England also left policy unchanged.

Markets currently anticipate a slower pace of monetary easing than previously expected.

Outlook

The global economic outlook remains broadly constructive, although the investment environment is becoming increasingly complex.

Economic growth across most developed economies is expected to remain close to long‑term trend levels during 2026. Corporate earnings remain strong and financial conditions remain supportive.

However, several structural themes are likely to shape market dynamics over the coming year including the continued expansion of artificial intelligence, persistent inflation pressures and rising geopolitical risks. Our central scenario is for the middle East conflict to resolve relatively quickly and for energy prices to return to pre-conflict level within 6-12 months. This appears to be the conclusion of current energy futures markets.

For Australian investors, the key domestic challenge remains balancing resilient economic growth with persistent inflation pressures. Equity market leadership may continue to broaden toward value, cyclicals and international markets.

Overall, we remain cautiously constructive on risk assets but expect market volatility to remain elevated. Disciplined asset allocation, global diversification and exposure to high‑quality income‑generating assets remain critical in this environment.

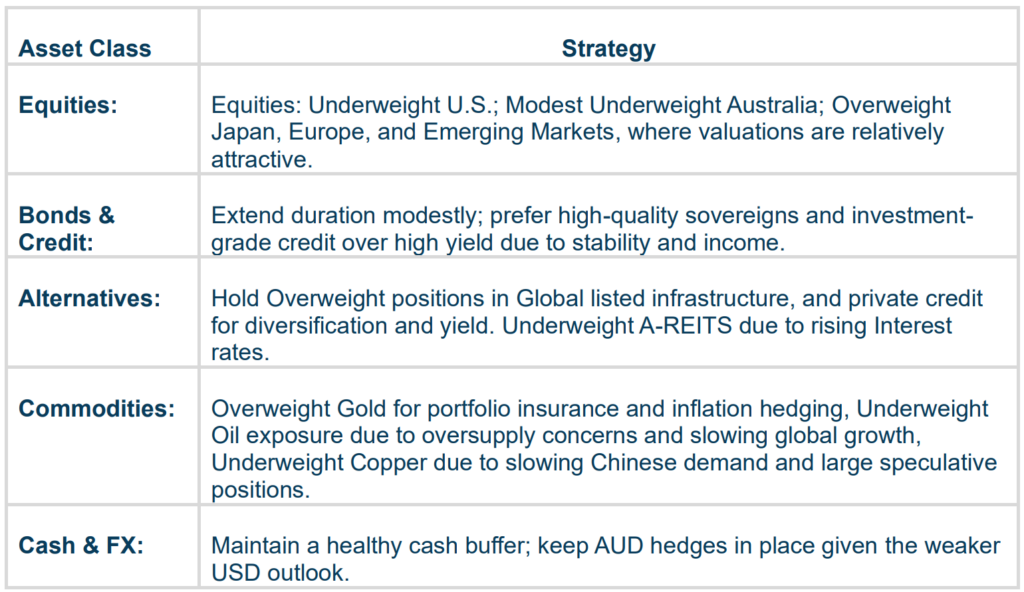

Portfolio Strategy & Asset Allocation