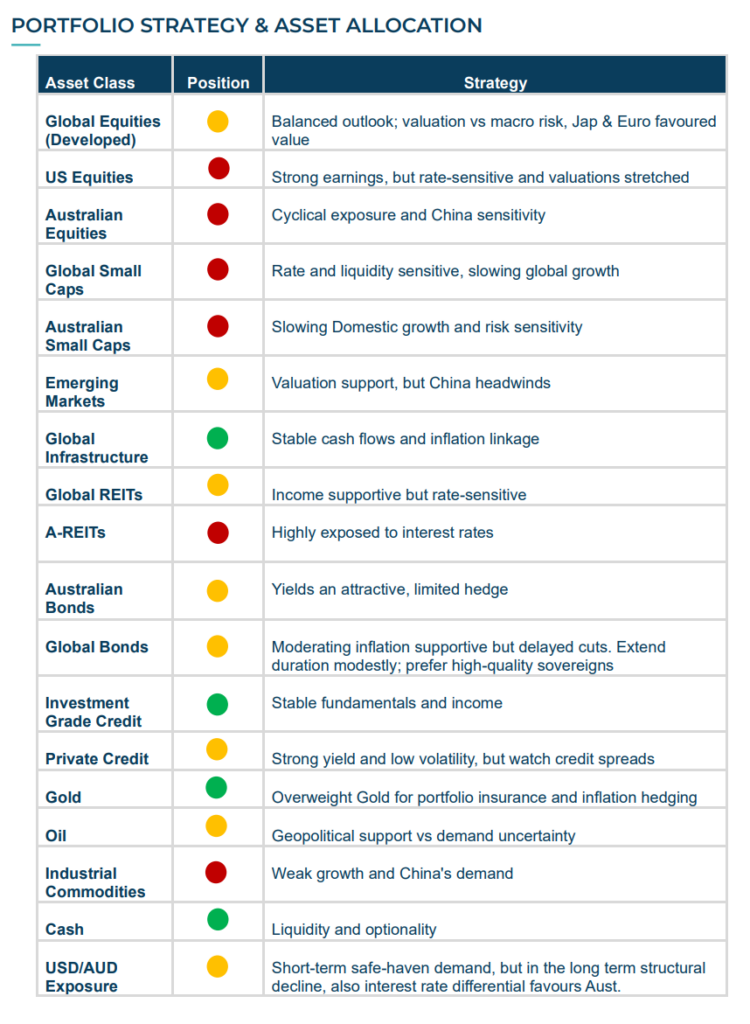

MONTHLY ECONOMIC & INVESTMENT REVIEW:

April 2026 marked a partial stabilisation in global financial markets following the sharp correction experienced in March. Risk sentiment improved modestly over the month as investors responded positively to signs that inflation pressures were continuing to moderate across several major economies. Equity markets recovered a portion of the prior month’s losses, while bond markets also stabilised as expectations for further aggressive policy tightening eased.

Despite the improvement in market conditions, volatility remained elevated relative to earlier in the year, reflecting ongoing uncertainty surrounding global growth, geopolitical developments and the path of monetary policy. Commodity markets were mixed, with energy prices remaining supported by ongoing disruptions to global supply chains and geopolitical tensions in the Middle East, while industrial commodities remained sensitive to slowing Chinese demand.

Overall, April represented a transition from the broad-based de-risking seen in March toward a more selective and cautious recovery environment. Markets continue to remain highly data dependent, with investors closely focused on inflation outcomes, labour market conditions and central bank communication.

Australian Equities

Australian equities recovered modestly during April, with the S&P/ASX 200 Total Return Index gaining approximately 2.2% for the month following the significant weakness experienced in March. Performance, however, remained uneven across sectors. Australian small companies outperformed large caps rising 3.3%.

The Financials sector stabilised as concerns around systemic credit stress moderated, although earnings expectations remain under pressure in a slower growth environment. Materials stocks experienced a partial rebound supported by resilience in iron ore prices and renewed optimism surrounding targeted Chinese stimulus measures.

Defensive sectors, including Healthcare and Consumer Staples, continued to outperform on a relative basis, reflecting investor preference for businesses with stable earnings profiles and stronger pricing power. Small capitalisation equities also recovered modestly but continued to lag larger capitalisation peers given their greater sensitivity to domestic growth conditions and financing costs.

While valuations have become more attractive following recent market weakness, the Australian market remains exposed to cyclical global growth risks and developments within China.

Global Developed Equities

Global developed equities delivered strong returns during April rising 4.4%, supported by improving investor sentiment and easing concerns around further monetary tightening. The US market was once again the major contributor rising a very strong 10.4%.

Technology and quality growth sectors recovered following the indiscriminate sell-off observed in March. Investor confidence was supported by relatively resilient corporate earnings and ongoing structural optimism surrounding artificial intelligence-related investment spending. However, market leadership remained concentrated in a relatively narrow group of high-quality companies with strong balance sheets and earnings visibility.

European equities underperformed broader developed markets as economic data across the Eurozone continued to weaken, reinforcing concerns around stagnating growth and fragile industrial activity. Japan continued to demonstrate relative resilience, supported by improving corporate governance trends and accommodative domestic financial conditions.

Despite the market recovery, global equity valuations remain sensitive to changes in bond yields and policy expectations, reinforcing the importance of maintaining a disciplined and selective investment approach.

Emerging Markets

Emerging market equities also bounced back rising 9.3% during April. Chinese equities remained volatile as investors continued to question the sustainability of the country’s economic recovery despite ongoing fiscal and monetary support measures. Property sector weakness, subdued consumer confidence and slower private sector investment continue to weigh on medium-term growth expectations within China.

Broader emerging markets also faced headwinds from a stronger US dollar environment and tighter global liquidity conditions. Nevertheless, select regions within emerging markets continue to demonstrate more resilient fundamentals, particularly economies benefiting from structural manufacturing shifts and improving domestic demand dynamics. Valuations across emerging markets remain relatively attractive compared to developed markets; however, near-term performance is likely to remain heavily influenced by global growth conditions and China’s policy response.

Real Assets – Property & Infrastructure

Global Real estate equities rose 7.4% during April following the sharp declines of 8.3% in March. Listed real estate recovered most of the losses in March as bond yields stabilised. However, the sector remains highly sensitive to interest rate expectations and refinancing conditions. Despite the bounce, Australian A-REITs continue to face pressure from elevated financing costs and weaker commercial property valuations, particularly within office-related exposures.

Unlisted real assets continue to exhibit relatively stable performance characteristics, supported by appraisal-based valuations and longer-duration income streams. However, valuation lag effects remain an important consideration, particularly within segments facing structural demand challenges.

Listed infrastructure rose 1.6% after only falling a comparatively low 2.7% in March and continued to demonstrate resilience, supported by defensive cash flow characteristics, inflation linkage and lower sensitivity to economic cycles relative to broader equity markets.

Global infrastructure remains one of our highest conviction allocations within diversified portfolios. The asset class continues to benefit from structural themes including electrification, energy transition, digital infrastructure demand and long-duration contracted revenue streams.

Fixed Income & Interest Rates

Fixed income markets stabilised during April, with both Australian (0.1%) and global bond (0.3%) markets generating modest positive returns as investors reassessed the likelihood of further policy tightening.

Inflation data across several developed economies continued to moderate gradually, although services inflation and wage pressures remain elevated relative to central bank targets. This reinforced expectations that monetary easing cycles are likely to remain gradual rather than aggressive.

Bond yields declined modestly over the month as markets increasingly priced the possibility that policy rates may be near their peak across most developed economies. Credit markets remained broadly resilient, with investment grade credit continuing to offer attractive risk-adjusted income opportunities relative to cash.

The fixed income outlook has improved modestly compared with earlier in the year, particularly as starting yields remain attractive and provide greater defensive characteristics than were available during the ultra-low-rate environment of previous years.

Commodities & Currencies

Commodity markets produced mixed performance outcomes during April. Gold prices declined modestly during April as safe-haven demand moderated, real bond yields stabilized and investors rotated back toward risk assets following the sharp risk-off environment experienced in March.

Oil prices remained volatile but elevated overall, reflecting ongoing supply chain disruptions and geopolitical tensions surrounding Middle Eastern shipping routes. Energy markets continue to remain highly sensitive to geopolitical developments, particularly around the Strait of Hormuz and broader OPEC supply dynamics.

Industrial commodities experienced mixed performance. Copper prices recovered modestly during the month, supported by supply constraints and longer-term electrification demand themes, although weaker Chinese construction activity continues to act as a headwind for bulk commodities.

The Australian dollar recovered from its March lows of USD $0.685 to close at USD $0.719 during April. Currency markets remained heavily influenced by shifting interest rate expectations and broader global risk sentiment.

Volatility & Market Sentiment

Market volatility moderated during April following the sharp spike observed in March, although volatility levels remain elevated relative to historical averages. The VIX Index declined materially over the month as investor confidence partially recovered and markets adjusted to the evolving macroeconomic environment.

Despite the improvement in sentiment, markets remain highly sensitive to economic data releases and central bank communication. Investors continue to balance improving inflation trends against concerns surrounding slowing global growth and earnings sustainability.

The moderation in volatility is encouraging; however, current conditions still reflect an environment of heightened macroeconomic uncertainty rather than a return to the low-volatility conditions experienced earlier in the cycle.

Global Macroeconomic Overview

The global economic backdrop remains characterised by moderating growth, increasing inflation risks and restrictive financial conditions. Economic activity across the United States has remained relatively resilient, supported by a still-healthy labour market and consumer spending, although forward-looking indicators continue to point toward slower momentum.

European economic conditions remain weaker, with manufacturing activity and business confidence continuing to soften. China’s economic recovery also remains uneven, with structural challenges in the property sector and subdued household demand limiting broader growth acceleration.

Global inflation continues to moderate gradually from the elevated levels experienced over recent years; however, progress remains uneven and increasingly vulnerable to geopolitical disruptions. A key emerging risk is the disruption to global oil supply chains resulting from the Iranian conflict and instability surrounding critical shipping routes such as the Strait of Hormuz, through which 20% of the world’s oil supply passes. Higher energy prices increase transportation, manufacturing and input costs across the global economy, creating secondary inflationary pressures that can flow through to consumer goods, freight and utilities. This dynamic is particularly concerning for central banks, as it risks slowing the pace of disinflation at a time when services inflation and wage pressures already remain persistent. As a result, the conflict has the potential to reinforce the “higher-for-longer” interest rate environment by delaying the timing and magnitude of future monetary policy easing globally.

Geopolitical risks remain elevated and continue to represent a key uncertainty for markets, particularly through their impact on energy prices, global trade flows and investor confidence.

Central Bank Policy

Monetary policy remained a central driver of market behaviour during April, although central bank communication became incrementally less hawkish compared with prior months.

The Reserve Bank of Australia, at the time of writing, increased rates by 25bp at the May meeting emphasising that inflation remains above target and that policy would need to remain restrictive for some time. This increase together with the two previous increases in February and March have effectively reversed the three rate cuts delivered during 2025, which had reduced the cash rate from 4.35% to 3.60% by August 2025. For the average Australian mortgage holder, this means borrowing costs have now returned to the same restrictive settings experienced prior to last year’s easing cycle. On an average new mortgage of approximately $736,000, the latest May increase alone is estimated to add around $117 per month in repayments, further pressuring household cash flows at a time when cost-of-living pressures remain elevated.

The US Federal Reserve kept rates on hold at 3.50 – 3.75% during April, marking the third consecutive meeting with no change. While inflation progress has improved modestly, the Federal Reserve continued to stress the importance of sustained evidence that inflation is returning toward target before considering policy easing.

Similarly, the European Central Bank and Bank of England maintained a cautious approach, reinforcing the broader global “higher-for-longer” interest rate environment. However, bond markets increasingly interpreted central bank communication as signalling that peak policy rates may now be close across most developed economies.

This evolving policy backdrop contributed to the stabilisation in both equity and bond markets during April, although policy uncertainty remains a significant source of market volatility.

OUTLOOK

The investment outlook has become more cautious following the sharp market correction in March, which underscored the increasing sensitivity of asset prices to macroeconomic and policy developments. While the global economy continues to demonstrate underlying resilience, the combination of elevated interest rates, moderating growth and heightened geopolitical risks suggests that volatility is likely to remain a defining feature of markets in the near term.

The recent repricing across equity markets reflects a clear shift in investor sentiment, as participants reassess both the sustainability of earnings growth and appropriate valuation levels within a higher interest rate environment. Although corporate fundamentals remain broadly intact, the margin for error has narrowed materially, particularly in sectors exposed to cyclical demand and global trade dynamics. At the same time, the delayed and uncertain timing of monetary policy easing reinforces the view that financial conditions will remain restrictive, limiting the potential for a sustained recovery in risk assets in the near term.

In this environment, portfolio construction requires a disciplined and risk-aware approach. Diversification across asset classes remains critical, particularly given the reduced effectiveness of traditional defensive assets observed during the month. There is an increased emphasis on quality across both equities and fixed income, favouring businesses and issuers with strong balance sheets, resilient cash flows and the ability to withstand a more challenging macroeconomic backdrop. Real assets, particularly infrastructure, continue to offer attractive diversification benefits, supported by stable income streams and partial insulation from short-term market volatility.

The correction in March may present selective opportunities as valuations adjust and dislocations emerge across markets; however, a cautious stance remains warranted until there is greater clarity on the trajectory of inflation, central bank policy and global growth. Maintaining elevated liquidity and preserving portfolio flexibility will be essential in allowing investors to respond effectively to evolving conditions. Overall, while the medium-term outlook remains constructive, the near-term environment calls for a measured and adaptive approach to asset allocation.