Private Credit as an Investment Asset Class

1. Introduction

Private credit, often referred to as private debt or direct lending, has emerged as one of the fastest-growing segments of the alternative investment universe. It involves non-bank institutions—such as asset managers, pension funds, and insurance companies—providing loans directly to borrowers through privately negotiated agreements rather than public bond markets. Over the past decade, the asset class has expanded substantially, driven by the retrenchment of traditional bank lending and investors’ search for higher yields in a low-interest-rate environment (Meketa, 2024; Cambridge Associates, 2024).

This paper explores the nature of private credit, the diversification benefits it provides, how it compares with conventional liquid asset classes, its pros and cons, and concludes with a recommendation regarding its role in a diversified portfolio of growth and income-producing assets.

2. What Is Private Credit?

Private credit broadly refers to debt investments that are not traded on public markets. The most common structures include direct lending, mezzanine financing, distressed debt, and special situations. The borrowers are typically private, middle-market companies seeking flexible capital solutions outside of the traditional banking system (Deutsche Bank Flow, 2024).

Private credit transactions are generally characterized by:

- Direct relationships between borrower and lender, allowing tailored loan terms.

- Floating-rate structures, with interest rates linked to a benchmark (e.g., SOFR, BBSY) plus a credit spread (Goldman Sachs Asset Management, 2024).

- Covenant protections and collateralization to manage downside risk (Cambridge Associates, 2024).

- Limited liquidity, as loans are often held to maturity with minimal secondary market activity (T. Rowe Price & Oak Hill Advisors, 2024).

According to Preqin and the Alternative Credit Council, the global private debt market exceeded USD 1.6 trillion by the end of 2023, reflecting continued institutional interest and strong fundraising momentum (PwC, 2023). The growth reflects both the pull factors (attractive returns and diversification) and push factors (bank deleveraging and regulatory constraints post-GFC).

3. Diversification Benefits of Private Credit

Private credit offers several unique attributes that can enhance diversification within a multi-asset portfolio.

- Low Correlation to Public Markets:

Private credit’s returns are derived from contractual cash flows rather than market trading dynamics. Consequently, it exhibits lower correlation with public equities and bonds, providing stability during periods of public market volatility (Cambridge Associates, 2024).

- Floating-Rate Income:

The majority of private credit instruments carry floating-rate coupons, making them resilient in rising interest-rate environments. This feature helps mitigate duration risk compared to fixed-rate bonds (Goldman Sachs Asset Management, 2024).

- Illiquidity and Complexity Premium:

Investors are compensated for accepting illiquidity, complexity, and limited transparency through higher yields. This spread premium, known as the illiquidity premium, is a primary source of excess return (Meketa, 2024).

- Structural Downside Protection:

Private credit typically benefits from strong covenant packages, seniority in the capital structure, and collateralization—features that help preserve capital in downturns (Deutsche Bank Flow, 2024).

- Access to Less Efficient Markets:

By focusing on smaller, less-followed borrowers, private credit managers can exploit inefficiencies unavailable in public debt markets, generating potential alpha (PwC, 2023).

In sum, private credit enhances diversification by combining higher yields, lower market correlation, and reduced duration exposure, which collectively improve portfolio resilience.

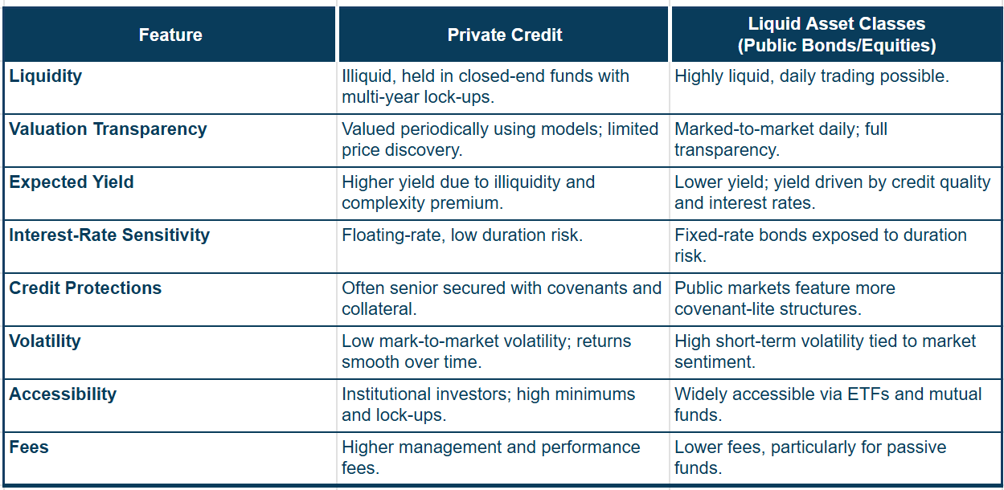

4. Comparison with Liquid Asset Classes

The table below summarizes key distinctions between private credit and conventional liquid investments:

Private credit therefore trades liquidity and transparency for yield and structural protection. While it provides a stable income stream and diversification, investors must accept longer holding periods and greater dependence on manager skill (Meketa, 2024).

5. Pros and Cons of Private Credit

Advantages:

- Attractive Yield:

Offers a 2–4% yield premium over broadly syndicated loans and public high-yield bonds (Federal Reserve Board, 2024).

- Floating-Rate Structure:

Income adjusts upward as benchmark rates rise, protecting against inflation and interest-rate risk (Goldman Sachs Asset Management, 2024).

- Diversification:

Exhibits lower correlation to traditional asset classes, improving portfolio risk-adjusted returns (Cambridge Associates, 2024).

- Strong Downside Protections:

Covenant protections and collateral enhance recovery prospects in default scenarios (Deutsche Bank Flow, 2024).

- Less Market Volatility:

Valuations are insulated from daily market swings, leading to smoother performance (Meketa, 2024).

Disadvantages:

- Illiquidity:

Limited secondary markets; investors face multi-year lock-ups with no early redemption (T. Rowe Price & Oak Hill Advisors, 2024).

- Opacity:

Private valuation models can obscure underlying credit deterioration until defaults occur (PwC, 2023).

- Manager Selection Risk:

Performance dispersion between top and bottom quartile managers is wide, emphasizing due diligence (Cambridge Associates, 2024).

- Fee Drag:

High management and performance fees can erode the illiquidity premium (Meketa, 2024).

- Credit and Economic Risk:

Borrowers are often smaller or leveraged firms; downturns can lead to higher defaults (Federal Reserve Board, 2024).

6. Expected Returns in Private Credit Relative to Cash Rates

From an asset allocation perspective, private credit should be evaluated not on an absolute return basis, but as a spread over the risk-free rate (cash). This spread represents the compensation investors receive for accepting credit risk, illiquidity, structural complexity, and manager execution risk.

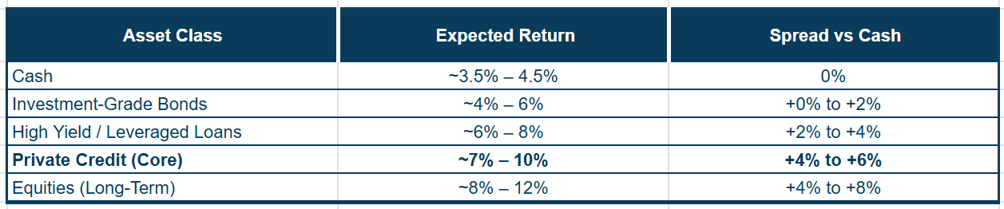

In current market conditions, a well-constructed private credit portfolio—particularly in senior direct lending strategies—should deliver a net return of approximately cash +4% to +6%. This equates to an absolute return range of roughly 7.5% to 10.5% p.a., assuming prevailing cash rates of ~3.5%–4.5%. This level of return is broadly considered the minimum threshold required to justify allocation, particularly when compared to liquid credit alternatives.

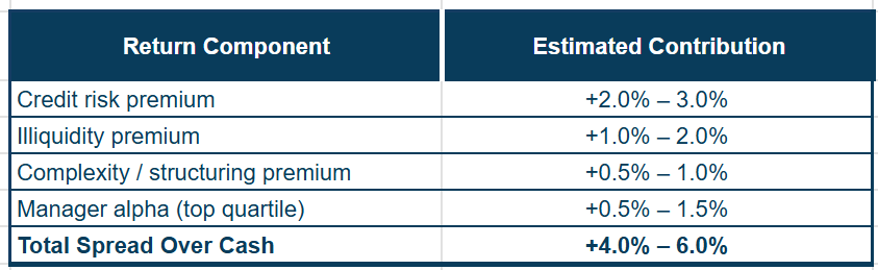

Return Composition: Sources of the Private Credit Premium

From an investor perspective, the illiquidity premium is the critical driver and must be sufficiently large to compensate for the inability to rebalance or exit positions in stressed environments. Manager alpha is also non-trivial, as dispersion between top and bottom quartile managers in private credit is significantly wider than in public markets.

Expected Returns by Strategy

The core allocation case for most portfolios sits within senior direct lending and unitranche strategies, where the balance between yield and capital preservation is most attractive. Higher-return strategies such as mezzanine and distressed debt introduce more equity-like risk characteristics and should therefore be treated as opportunistic or satellite allocations.

Relative Value: Private Credit vs Other Asset Classes

This positioning highlights the strategic role of private credit: it offers enhanced income relative to public credit, with lower volatility and greater structural protection than equities, but at the cost of reduced liquidity and transparency.

What Constitutes an Adequate Return?

A spread of +4% to +6% over cash should be viewed as adequate, but not excessive. Whether this is sufficient depends on several factors:

- Default and Loss Assumptions – Expected default rates of 1%–3% p.a. and recovery rates of 60%–80% are generally embedded within return expectations.

- Manager Quality – Private credit outcomes are highly dependent on underwriting discipline, sourcing capability, and covenant enforcement.

- Fee Structure – Management and performance fees can materially reduce net returns, making fee efficiency important.

- Fee Structure – Management and performance fees can materially reduce net returns, making fee efficiency important.

Cyclical Considerations

From a macroeconomic perspective, private credit is most attractive when spreads are wide, banks are retrenching from lending, and underwriting standards remain disciplined. Conversely, the asset class becomes less compelling when excess capital compresses spreads and covenant quality deteriorates.

In the current post-rate-hiking environment, private credit remains structurally attractive because higher base rates support strong absolute income levels, while traditional bank lending remains constrained. However, increasing institutional inflows into the sector may compress future returns over time.

Portfolio Implications

From a portfolio construction perspective, several conclusions emerge:

- Private credit has a legitimate role as part of the income-generating allocation within a diversified portfolio.

- The asset class should complement, rather than replace, liquid fixed income due to its illiquid nature.

- A strategic allocation of approximately 5%–10% appears appropriate for many diversified portfolios.

- Manager selection remains the key determinant of long-term success.

- Investors should remain disciplined in assessing whether the spread over cash remains adequate relative to liquidity and credit risks.

Overall, the minimum acceptable hurdle rate for private credit should be considered:

Cash rate +4% to +6% (net of fees)

At current cash rates of approximately 4%, this implies target returns of roughly 8%–10% p.a. Returns materially below this range suggest investors are not being sufficiently compensated for illiquidity, credit risk, and structural complexity.

7. ASIC Investigation into Australia’s Private Credit Sector

The rapid growth of Australia’s private credit market has increasingly attracted regulatory attention, culminating in the Australian Securities and Investments Commission’s (ASIC) release of REP 814: Private Credit in Australia in September 2025 and the subsequent REP 820: Private Credit Surveillance Report in November 2025 (Australian Securities and Investments Commission [ASIC], 2025a; ASIC, 2025b). ASIC’s investigation was initiated in response to the substantial expansion of private capital markets, increasing participation from retail investors, and rising concerns surrounding governance, valuation transparency, liquidity management, and investor protection.

ASIC (2025a) noted that private markets had expanded significantly in Australia and globally, while activity in public capital markets—including IPOs and listed equity issuance—had declined. The regulator became increasingly concerned that private credit markets were evolving faster than existing disclosure standards and regulatory oversight frameworks. In particular, ASIC highlighted that many private credit structures were opaque, difficult for retail investors to fully understand, and often exposed to concentrated property-development and commercial real-estate lending risks.

The investigation, led by infrastructure investment executive Richard Timbs and former bank chief risk officer Nigel Williams, sought to assess the size, governance practices, operational standards, and emerging risks within Australia’s private credit market (ASIC, 2025a). ASIC’s broader objective was to determine whether current industry practices remained consistent with investor-protection obligations and whether additional regulatory guidance may be required as the sector matures.

One of the most significant findings from the review was the wide variation in governance and operational standards across the industry. ASIC identified examples of both “better” and “poorer” practices, particularly regarding valuation processes, conflict management, disclosure quality, and liquidity frameworks (ASIC, 2025b). The regulator expressed concern that some managers lacked sufficiently independent valuation methodologies and relied heavily on internal deal teams to assess the value of illiquid loans. ASIC warned that this practice could increase the risk of inflated asset valuations and delayed recognition of impairments during periods of credit stress.

Another key finding related to fee disclosure and transparency. ASIC (2025b) identified cases where private credit funds provided insufficient disclosure regarding the spread earned between borrower interest rates and investor returns, as well as the extent of additional fees generated through establishment charges, repayment penalties, and distressed restructuring arrangements. The regulator concluded that some investors may not fully understand the drivers of portfolio returns or the total level of manager compensation embedded within fund structures.

ASIC also highlighted concerns surrounding related-party transactions and conflicts of interest. In several structures reviewed, affiliated entities performed multiple roles across the lending process, potentially compromising governance independence and increasing risks to investors during periods of market stress (ASIC, 2025b). The regulator warned that these issues could become more pronounced if economic conditions deteriorate, liquidity weakens, or default rates rise.

Importantly, ASIC did not conclude that private credit itself is inherently problematic. Rather, the regulator acknowledged that private credit can play a valuable role in complementing the traditional banking system by increasing access to capital and supporting economic activity (ASIC, 2025a). However, ASIC stressed that stronger governance standards, improved transparency, enhanced valuation independence, and more robust risk-management frameworks will be necessary as the sector continues to institutionalise.

From an investment perspective, ASIC’s findings reinforce the importance of manager selection, underwriting discipline, governance quality, and liquidity management within private credit portfolios. While the asset class continues to offer attractive yield and diversification benefits, the investigation highlighted that not all market participants operate to institutional-grade standards. Consequently, investors must undertake enhanced due diligence around valuation policies, fee structures, liquidity terms, covenant protections, and conflict-management procedures before allocating capital.

Overall, ASIC’s investigation represents a significant milestone in the maturation of Australia’s private credit industry. The review suggests that the sector is likely to face increasing regulatory scrutiny in coming years, particularly as retail participation expands and private markets become more systemically important within the Australian financial system.

8. Fee Structures in Private Credit Funds

Private credit fee structures are generally more complex and higher than traditional listed fixed-income products due to the intensive nature of loan origination, underwriting, structuring, monitoring, and workout management. However, fee transparency has become an increasing area of focus for institutional investors and regulators, particularly following ASIC’s recent surveillance reviews of the Australian private credit market (Australian Securities and Investments Commission [ASIC], 2025a; ASIC, 2025b).

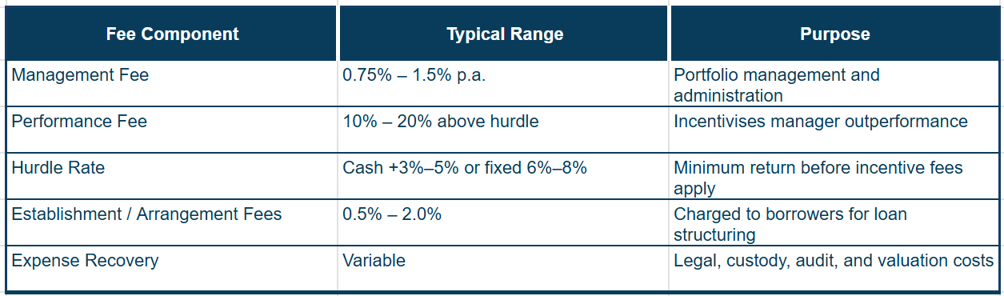

A typical private credit fund will include a management fee, performance fee, and additional transaction-related costs. The table below outlines standard market ranges:

For most quality senior direct lending funds, a management fee of approximately 1.0% p.a. is generally considered fair. Higher-risk strategies such as distressed debt or opportunistic lending may justify higher fees due to increased complexity and restructuring involvement. Performance fees are more contentious in private credit than in private equity because the asset class is primarily designed to generate stable income rather than outsized capital gains. Consequently, performance fees are generally viewed as reasonable only where managers consistently generate excess net returns above a meaningful hurdle rate.

From a portfolio-construction perspective, the most important metric is the net spread over cash after fees and defaults. A fund generating gross returns of 11% may ultimately deliver only 8%–9% net to investors once fees and impairments are deducted. The ASIC report (2025b) also highlighted concerns around inadequate disclosure of borrower arrangement fees, restructuring charges, and related-party transactions, warning that some investors may not fully understand the total level of manager compensation embedded within fund structures.

Ultimately, fees should be assessed relative to underwriting quality, downside protection, and net risk-adjusted returns delivered to investors. If a private credit manager charges management fees of approximately 1.5% in addition to high performance fees, yet delivers returns broadly comparable to liquid leveraged loans or public high-yield credit markets, then the illiquidity premium may not adequately compensate investors for the additional complexity, reduced transparency, and limited liquidity associated with the asset class. In these circumstances, investors may be assuming materially greater liquidity and operational risks without receiving a sufficient enhancement in net returns. Consequently, the justification for allocating capital to private credit becomes weaker, particularly when lower-cost and more liquid alternatives are capable of delivering similar income outcomes.

9. Recommendation

The fundamental question is whether private credit deserves a place in a diversified portfolio, or if its risk-return characteristics can be replicated more efficiently through liquid proxies such as leveraged loans, high-yield bonds, or listed Business Development Companies (BDCs).

Case for Inclusion:

Private credit can play a legitimate role within a diversified growth-and-income portfolio, particularly for investors with long-term horizons and the capacity to tolerate illiquidity. Its appeal lies in its:

- Superior yield relative to public bonds.

- Floating-rate protection against inflation and interest-rate increases.

- Low correlation and reduced volatility relative to public markets.

- Potential for downside protection through covenants and senior secured positions (Goldman Sachs Asset Management, 2024).

Caveats:

However, private credit’s advantages come with trade-offs:

- Liquidity constraints limit flexibility in portfolio rebalancing.

- Valuations are less transparent, increasing uncertainty in downturns (T. Rowe Price & Oak Hill Advisors, 2024).

- Excess capital inflows may compress spreads, reducing future returns (PwC, 2023).

- High fees can diminish net yields compared to passive liquid alternatives (Meketa, 2024).

Portfolio Role:

For investors seeking stable income and total-return enhancement, a 5–10% strategic allocation to private credit appears reasonable (Cambridge Associates, 2024). The allocation should be implemented through established managers with robust track records, disciplined underwriting standards, and diversified portfolios across sectors and geographies.

For investors with shorter investment horizons or liquidity needs, liquid proxies—such as floating-rate bank loan funds, high-yield ETFs, or listed private credit vehicles—may offer a more efficient way to capture similar risk-return characteristics (Federal Reserve Board, 2024).

10. Conclusion

Private credit represents a credible and increasingly institutionalized component of the alternative investment landscape. It delivers differentiated exposure, a potential yield premium, and portfolio diversification benefits that justify its inclusion in a well-balanced, growth-and-income-oriented portfolio. Nonetheless, its success depends heavily on manager quality, credit cycle positioning, and investor tolerance for illiquidity. When accessed prudently, private credit can complement traditional fixed-income and equity exposures; however, for liquidity-constrained investors, its risk/return trade-off may be more efficiently replicated through liquid credit markets.

References

Australian Securities and Investments Commission. (2025b). REP 820: Private credit surveillance report: Retail and wholesale surveillance. ASIC.

Cambridge Associates. (2024). Private credit strategies: An introduction.

Deutsche Bank Flow. (2024). Private credit: A rising asset class explained.

Federal Reserve Board. (2024). Private credit characteristics and risks.

Goldman Sachs Asset Management. (2024). Understanding private credit.

Meketa Investment Group. (2024). Private credit primer.

PwC. (2023). The private credit report.

T. Rowe Price & Oak Hill Advisors. (2024). An introduction to private credit.